Can a business get a mortgage in the UK?

Can a business take out a mortgage? The short answer is yes, a company can get a mortgage, and in many cases, a business mortgage can be a smarter long-term choice than renting. However, securing a business mortgage involves different eligibility criteria, interest rates and repayment terms than personal home loans.

Questions like ‘can a business get a mortgage UK?’, ‘can a company get a mortgage?’ or ‘can I get a mortgage through my business?’ all come up regularly. The short version is that businesses can get mortgages for commercial purposes, but they generally cannot use a business mortgage to buy the directors’ personal home. If you’re a limited company director, there are specific lending criteria and considerations to be aware of, as lenders often assess your income, experience and documentation requirements differently compared to other applicants.

If you’re wondering whether a business mortgage, a commercial loan or using a business loan to buy property is the right option for you, it helps to see how the different routes work in 2026. Company directors may face additional complexities and should ensure they meet the lender’s lending criteria, as these can vary depending on business structure and intended property use.

In this article, we’re going to discuss how you can:

- Understand what a business mortgage is and when a business can have a mortgage on a property

- Compare business mortgages with other types of commercial property finance and business loans

- Follow the key steps to get a business mortgage in the UK and improve your chances of approval

What Is a Business Mortgage?

A mortgage is a loan for the cost of a property. In the case of a business mortgage, the borrowing is in the name of the business, and the lender expects the property to be used wholly for business purposes. A business mortgage can also be used to purchase new premises for the company.

A business can use a mortgage to acquire a property that it will occupy itself, to refinance an existing building and release equity or to fund redevelopment work that adds value or functionality to the site. The key point is that the mortgage is linked directly to a specific property used as security.

You may also ask, ‘can a business get a residential mortgage?’ The answer is yes, as long as you use the residential property for commercial purposes such as buy-to-let, serviced apartments or staff accommodation. In that case, lenders usually treat it as a form of commercial or investment property lending. Choosing the right mortgage product is important based on the intended use of the property.

So if you want to borrow toward the cost of an apartment complex to generate rental income, a commercial mortgage is a suitable option, and there are specialist business mortgages for residential property of that kind. Trends in the property market can influence the types of mortgage options available and may affect lender requirements for investment properties.

If you want to borrow through your business to finance the purchase of your personal home, however, this isn’t possible. You cannot simply put your own house through a limited company to avoid residential rules, and lenders will not usually accept that structure for a home you live in.

What Can a Mortgage Do for Your Business?

A business mortgage can deliver several benefits to your business beyond simple ownership.

Over the life of the loan, your monthly payments are gradually buying an asset for your balance sheet rather than paying a landlord. At the end of the mortgage period, your business owns the property outright, which can strengthen your net worth and give you more control over your premises.

During the term, you’re often paying less each month than you would in rent for comparable space, especially in prime locations. In many cases, the total spent on mortgage interest over a decade or more works out lower than the rent you would have paid in the same period.

A mortgage also gives you more options. As your equity in the property grows, you can release some of that equity by refinancing if you need capital for expansion, acquisitions or other projects. Some lenders may allow you to access a larger mortgage by considering retained profits in addition to your standard income, which can significantly increase your borrowing capacity. If the property’s value increases, the value of your investment rises as well, which can improve your gearing and borrowing power. Retained profits can also improve your borrowing capacity, especially for company directors or self-employed applicants.

Financial forecasting becomes simpler with a mortgage because repayments are usually less prone to variation than rent, particularly under fixed or tracker rate structures. Opting for a fixed interest rate can provide stability in your monthly payments, helping you plan your finances with greater confidence. Finally, interest rates for commercial mortgages are usually lower than many other types of business finance, thanks to the high value of the property the loan is secured against.

Taken together, these are strong reasons why many owners decide that a business mortgage is worth exploring.

How to Qualify for a Business Mortgage

To secure a business mortgage, lenders assess several factors, including:

- Business credit score: Lenders prefer businesses with a strong credit rating, typically above 700.

- Trading history: Most lenders require at least two years of profitable trading records, and at least two years of accounts to demonstrate financial stability.

- Deposit requirements: A commercial mortgage usually requires a minimum 20-30% deposit.

- Loan-to-value ratio (LTV): The lower the LTV, the better the loan terms.

- Business profitability: Lenders evaluate net profit margins to determine affordability.

Self-employed individuals or those running their own business may need to provide more evidence of income, such as accounts covering multiple tax years, to satisfy lender requirements.

If your business is newer, lenders may tighten these requirements and ask for higher deposits or personal guarantees. Providing accounts and thorough documentation can help improve your chances of approval.

If your business lacks trading history, consider a business loan to buy property instead of a traditional mortgage, or look at other secured business loans UK UK-based lenders offer while you build up your track record.

What Types of Commercial Mortgages Are There?

There are several types of property finance, from the simple commercial mortgage through to more elaborate options designed to target specific situations. The mortgage application process can vary depending on the type of finance you choose, and many lenders have different requirements and ways of assessing eligibility. Understanding these options helps you decide not just ‘can a business get a mortgage?’ but also which type of business mortgage or property loan fits best. When comparing different types of property finance, keep in mind that many lenders assess applications differently. Some may use an average of several years’ income, while others focus on the most recent year. So, it’s important to understand their specific lending criteria before applying.

Commercial mortgages

This type of finance is a loan secured against a property which will be used solely for business activities, or which represents a business in its entirety.

Commercial mortgages are a great choice if your business wants to transition away from leasing its premises or if you are looking to establish a buy-to-let business model and hold investment property in your company.

A business can also take out a mortgage on all or part of a property it already owns to unlock the capital it represents. This is referred to as refinancing, and is a common route when owners want to raise funds for expansion without selling the building.

Portfolio finance

Whereas a commercial mortgage sees a loan secured against one property, portfolio finance allows you to borrow against two or more properties under a single facility.

The cash borrowed can be used to acquire more property, develop one or more of the properties within the portfolio, or simply to free up some of the capital locked inside.

Because the value of the portfolio is high and the risk is spread, portfolio finance usually offers lower interest rates than standalone commercial mortgages. It can be particularly useful for landlords and investors holding multiple units within a company structure.

Bridging loans

If you need short-term finance to bridge the gap between acquiring a new property and being approved for a mortgage that entirely covers its cost, a bridging loan can help. Equity in a property you already own is unlocked and used as a down payment for another purchase.

Whereas mortgage terms can span several decades, the upper limit for bridging finance is usually one year. Learn more about bridging loans to see if it might be something right for you.

Development finance

This type of loan is for businesses that want to develop a new property or redevelop an existing property. Terms are tailored toward this outcome and will differ slightly from those you would see if you borrowed the equivalent amount through a standard commercial mortgage. Learn more about development finance.

Mezzanine finance

This funding type is a hybrid of debt and equity finance and tops up funding shortfalls on high-cost property projects. If you have secured the majority of the investment you need through a mortgage, mezzanine finance could provide the remainder of what is required to get the project over the line.

In larger deals, it’s common to see a blend of commercial mortgage, mezzanine finance and equity, often with separate security and pricing for each layer.

How to Get a Business Mortgage in the UK

Securing a business mortgage can be a smart move if you’re looking to purchase commercial premises instead of leasing. Whether you’re planning to buy an office, shop, warehouse or other commercial asset, here’s a step-by-step guide to getting a business mortgage in the UK. Some lenders now offer an instant decision on your mortgage application, allowing you to know your eligibility and move forward with funding much faster.

It’s worth noting that approval times and requirements can vary significantly between lenders, especially as lending criteria have evolved since the 2007 financial crisis.

1. Assess your requirements

Start by determining the type and location of property you want to buy, how much deposit you can provide and what monthly repayments you can realistically afford based on your current cash flow.

Being clear about your budget and target properties upfront will save time later and help you explain to lenders exactly what you need.

2. Check your eligibility

Lenders will look at several factors, including your business’s trading history, company credit rating, director credit profiles, business structure and profitability. They’ll test affordability using your historic and forecast profits to ensure the mortgage is sustainable.

If you’re asking, ‘can my business get a mortgage?’ or ‘can a business get a mortgage loan at all?’, this eligibility stage is where you will find out how lenders view your risk profile.

3. Get a property valuation

Most lenders will require a formal property valuation to assess market value, condition, future potential and suitability for commercial use.

This valuation supports their lending decision and sets the maximum loan-to-value they’re willing to offer.

4. Prepare your documents

You’ll need recent business accounts, bank statements, proof of ID and address for directors and sometimes a business plan or forecast if you are applying as a new venture or start-up.

For a new business mortgage, lenders will lean more heavily on projections and personal guarantees, so the quality of your paperwork makes a real difference.

5. Apply through a lender or broker

You can apply directly with commercial mortgage lenders or work through a broker who has access to a wider panel. A broker can help match you with lenders that are more flexible or niche, particularly if you’re in a specialist sector or have a short trading history.

6. Undergo affordability and risk checks

Lenders will conduct credit checks on both the business and the directors, affordability analysis on your profit and loss and debt service ratios, and legal checks on the property itself.

This stage may involve questions about your forecasts, existing debts and how you plan to use the building.

7. Receive an offer and complete

If approved, you’ll receive a mortgage offer. Once legal due diligence is complete, including searches and contracts, funds are released and you complete the property purchase.

At that point, your business has a mortgage secured against the property and regular repayments begin.

Mortgage Terms and Conditions: What to Watch For

When you’re considering a commercial mortgage for your business, it’s vital to look beyond the headline interest rate and monthly repayments. The terms and conditions of your mortgage agreement can have a significant impact on your business finances, flexibility and long-term costs. Understanding these details will help you avoid unexpected expenses and ensure your commercial property finance supports your business goals.

Early repayment fees

Early repayment fees, sometimes called early redemption charges, are costs you may incur if you pay off your commercial mortgage before the end of the agreed term. Most lenders include these fees to compensate for the interest they lose when a loan is repaid early. Typically, early repayment fees are calculated as a percentage of the outstanding loan, often ranging from 1% to 5%. For example, if you have a £500,000 commercial mortgage and the early repayment fee is 3%, you could face a £15,000 charge for settling the loan ahead of schedule.

It’s important to check the specific terms with your lender, as some specialist lenders offer more flexible terms, including reduced or even no early repayment fees. If you anticipate the possibility of refinancing, selling the property or repaying your mortgage early, prioritise lenders that provide flexible terms to avoid unnecessary costs. Always ask about early repayment fees before committing to a mortgage, as these charges can significantly affect your overall financial planning.

Flexibility and special clauses

Commercial mortgages can offer a range of flexible terms and special clauses designed to support business owners through different stages of growth. For instance, some lenders may provide a capital repayment holiday, allowing you to pause repayments for a set period, which is an option that can be invaluable for new businesses or during periods of cash flow pressure. Other flexible features might include the ability to make overpayments without penalty, or to switch between fixed and variable interest rates as your needs change.

It’s also common for commercial property finance agreements to include clauses related to eligibility criteria, such as minimum trading history, deposit requirements and acceptable credit history. These factors can influence not only your approval chances but also the terms you’re offered. Working with a mortgage broker can help you navigate these options and identify lenders who are willing to accommodate your specific circumstances, whether you’re a limited company, sole trader, or have a limited trading history.

When reviewing your commercial mortgage terms and conditions, pay close attention to:

- Eligibility criteria: Make sure you understand the lender’s requirements for credit history, trading history and deposit size.

- Interest rates: Compare fixed and variable rates, and consider how changes in interest rates could affect your monthly repayments.

- Loan terms: Check the length of the loan, repayment structure, and any flexibility, such as overpayments or capital repayment holidays.

- Fees and charges: Be aware of all associated costs, including arrangement fees, valuation fees and early repayment fees.

- Credit checks: Know how lenders will assess your creditworthiness and how this might impact your credit report.

- Tax implications: Consider how your mortgage will affect your taxable income and whether you can claim tax relief on interest payments.

By thoroughly reviewing the terms and conditions of your commercial mortgage, you can ensure you’re making an informed decision that aligns with your business’s needs and future plans. Consulting a mortgage broker can help you find the right solution, negotiate flexible terms and secure the commercial property that will help your business thrive. With careful planning and the right finance in place, you’ll be well positioned to grow your business and make the most of your property investment.

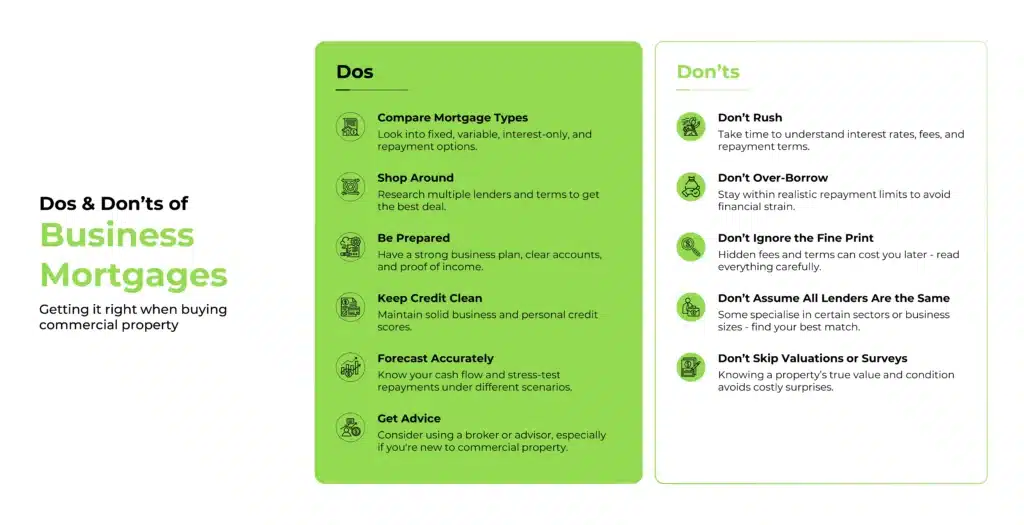

The Dos and Don’ts of Business Mortgages

There are some key dos and don’ts when taking out a business mortgage, and it’s worth thinking through these before you sign anything.

You should research different types of commercial mortgages and lenders rather than accepting the first offer you receive. Take time to compare interest rates, fees and repayment schedules and make sure they match your cash flow. Prepare a solid business plan, clear financials and proof of cash flow so you can meet the lender’s requirements confidently. Having at least one year’s trading history can also significantly improve your chances of approval, as many lenders include this in their lending criteria.

You should also focus on maintaining a good credit rating for both the business and its directors, because this will increase your chances of approval and help you secure more attractive terms.

On the other hand, you should not skim the fine print or rush the process. Ignoring clauses on early repayment, covenants or default can cost you later. Be aware that self-certification mortgages, which allowed borrowers to secure a mortgage without providing income proof, are no longer available due to past misuse and regulatory changes following the 2007-2009 financial crisis. You should also avoid overburdening your business by borrowing more than you can realistically repay, even if a lender is willing to advance that amount. A conservative, sustainable mortgage is far better than aggressive borrowing that puts your company at risk.

How Does a Business Mortgage Compare to a Personal Mortgage?

A business mortgage and a personal mortgage differ in several key ways. At a basic level, a personal mortgage is designed for buying a home you live in, while a business mortgage is designed for buying commercial property or investment property held in a company or business structure.

Typical differences include:

- Purpose: Business mortgages are used for buying commercial property for business use or business-backed investment, while personal mortgages are for purchasing a home for personal use.

- Deposit required: Business mortgages typically need 20-40% deposits, whereas residential mortgages can be available with 5-15% deposits for owner occupiers.

- Interest rates: Business mortgage rates are generally higher than personal mortgages, which benefit from lower perceived risk and consumer regulation.

- Loan terms: Business mortgages tend to run for 5-25 years, compared with 15-30 years for many personal mortgages.

- Eligibility criteria: Business mortgage eligibility is based on business finances, revenue and credit, while personal mortgage eligibility is based on personal income and credit history.

- Lender options: Business borrowers may use high street banks and specialist lenders, while personal borrowers can also use building societies and mainstream mortgage brokers.

If you run a limited company, some lenders allow a business mortgage to be taken in the company’s name, helping to separate personal and business finances. That is often the structure used when people ask, ‘can I buy a house in my business name?’ for a property that will be let out rather than lived in.

Case Study: How One Business Secured a Commercial Mortgage

Jane, the owner of a growing e-commerce company, wanted to purchase a warehouse to streamline logistics.

With a £200,000 deposit and a solid financial history, she secured a £500,000 mortgage with an interest rate of 4.5%. By owning her premises instead of leasing, she saved £1,500 per month compared to her previous rental costs.

Key takeaways from her experience include the importance of a strong credit score and financial history for obtaining better interest rates, the fact that owning a business property can be cheaper than renting over time, and the role specialist lenders can play in providing more flexible terms for SMEs.

In effect, Jane’s story answers the question ‘can a business get a mortgage loan that truly saves money?’ with a clear yes, as long as the numbers and the strategy are sound.

Key takeaways on business mortgages for companies

- A business can get a mortgage in the UK for commercial or investment property, but you cannot usually use a business mortgage to finance your own home

- Lenders look closely at trading history, profitability, deposit and credit, so preparation and realistic affordability are key if you want your company to get a mortgage

- There are multiple ways to finance property, from standard business mortgages to bridging and development finance, so the right structure depends on your plans for the building

To sum up, a business mortgage can help you finance the acquisition of one or more properties that you will use for commercial purposes. This could be office space where your primary business activities will take place, or it could be an apartment complex intended to generate rental income of its own.

Other types of commercial property finance exist, too. They can help you fund development, bridge temporary finance shortfalls or top up funding gaps where a mortgage alone is not enough.

Applying for a business mortgage is relatively straightforward, but not all business owners meet the criteria required.

Funding Guru prides itself on taking into account the plans of a business as well as its history, so if you are a business owner struggling to get a commercial mortgage, get in touch today.

FAQ about Business Mortgages for Limited Companies

Can your startup get a business mortgage?

Yes, but it is more challenging than for a well-established firm. Startups usually need a larger deposit, often 30-40%, and personal guarantees from the owners to secure a loan. Lenders will lean more on your business plan, forecasts and personal credit histories. Alternative funding, such as secured business loans UK-based lenders provide, may be more accessible once your trading record is longer.

Is a business mortgage usually cheaper than renting commercial premises?

In the long term, a business mortgage can work out cheaper than renting comparable premises. While the initial costs of buying commercial property are higher, including stamp duty, legal fees and a deposit, monthly mortgage payments are often lower than rental rates, especially in high-demand locations. Over time, you’re also building equity rather than paying a landlord, which improves the overall economics.

How much deposit do you need for a business mortgage in the UK?

Most lenders require at least 20-30% of the property’s value as a deposit on a business mortgage. For higher risk businesses, new ventures or those with limited trading history, this can increase to 40% or more. If you have a lower deposit, you may need to look at alternative financing options such as a secured business loan or bridging loan while you build up more equity or savings.

Can you get a mortgage through your business for your home?

You generally cannot get a business mortgage through your company to purchase a home you plan to live in. Lenders treat owner-occupied residential property differently from commercial or investment property, and they expect personal residential mortgages to be in your own name. If you’re asking ‘can I get a home loan through my business?’ for your main residence, the answer is almost always no.

Can you use a business loan to buy property instead of a mortgage?

Yes, it is possible to use a business loan to buy property, but it is less common than using a dedicated business mortgage. Business loans are usually unsecured or short-term finance, while mortgages are designed specifically for property purchases and tend to offer lower interest rates over longer repayment terms. If you are considering buying property, a commercial mortgage will typically be a better and more cost-effective solution, with a business loan mortgage structure only used in more niche situations.