Hire purchase in 2026: what you need to know

The British financial landscape is as diverse as it is complex.

Among the many financing options available to businesses, hire purchase stands out as a popular choice in 2026 for vehicles, machinery and other essential assets. There are several car finance options to consider, including other car finance options such as personal contract purchase (PCP) and leasing, each with its own features and benefits. But like any financial instrument, understanding the advantages and disadvantages of hire purchase is crucial if you want to avoid expensive mistakes and choose the right funding mix for your business.

If you’re asking ‘what is hire purchase?’, ‘what are the advantages of hire purchase?’ or weighing up the hire purchase pros and cons against leasing or loans, you’re in the right place. When considering finance options, it’s important to understand the different types of car finance available, as each can impact your business’s cash flow and long-term financial planning.

In this article, we’re going to discuss how to:

- Understand the hire purchase meaning and how a typical agreement works in practice

- Evaluate the key advantages and disadvantages of hire purchase for buyers and sellers

- Decide when hire purchase in financial services makes sense as part of your funding strategy

- Compare hire purchase deals with other car finance options, including personal contract purchase (PCP) and leasing

What is Hire Purchase?

Hire purchase meaning in simple terms

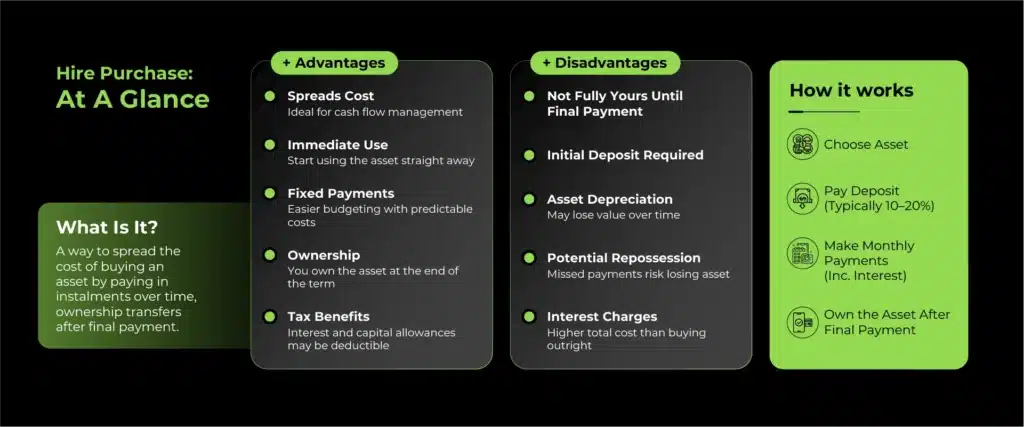

Hire purchase (HP) is a form of asset finance where a buyer pays for a product in instalments. Once all payments are completed, the ownership of the product transfers from the seller to the buyer. Commonly used for acquiring cars, machinery and other high-value items, it allows the buyer to use the product while they’re still paying for it.

In other words, HP lets you spread the cost of a large purchase while still having day-to-day use of the asset. That basic structure is at the heart of most advantages of hire purchase, but it also creates some of the disadvantages of hire purchase if the deal is not managed well.

How hire purchase works step by step

Although each provider has its own paperwork, most hire purchase agreements follow the same pattern:

- You agree the price of the asset and the HP terms with the seller or finance company, including deposit, interest rate and length of contract.

- You usually pay an initial deposit, then fixed monthly instalments over an agreed period.

- During the term, you have use of the asset, but legal ownership remains with the lender.

- Once you’ve made the final payment (and sometimes a small option to purchase fee), legal ownership transfers to you.

This structure makes hire purchase particularly attractive for businesses and individuals who need the asset to generate income, but don’t want to tie up cash in a full upfront payment.

Why Businesses Use Hire Purchase

Asset accessibility

For many businesses, especially startups and SMEs, acquiring high-value assets such as machinery, vehicles or specialised equipment can be daunting from a financial point of view. HP provides a pathway to access these assets without the need for a large upfront payment.

This means businesses can utilise essential assets to generate revenue, even as they’re still in the process of purchasing them. It’s one of the most important advantages of hire purchase to the buyer and part of the wider importance of hire purchase in asset finance.

Cash flow management

In the unpredictable ebb and flow of business finance, maintaining positive cash flow is a must. By opting for HP, businesses can better manage their cash flow, ensuring they aren’t depleting their reserves on a single high-value purchase.

Instead, the cost is spread over a more manageable period, allowing for better financial planning and allocation of resources to other critical areas such as staff, marketing or working capital. This is one of the key benefits of hire purchase compared with paying outright.

Asset maintenance and upgrades

Some HP agreements come with provisions for maintenance by the seller until the asset is fully paid off. Additionally, businesses can choose to upgrade to newer models or versions through new HP agreements, ensuring they always have access to the latest technology or equipment.

Handled sensibly, this can help a business stay competitive without constant large capital outlays, although it does mean you’re often in a cycle of ongoing commitments rather than owning outright with no further payments.

Hire purchase isn’t just about acquiring assets; it can be a strategic move, allowing businesses to operate efficiently, stay competitive and grow without being hindered by immediate financial constraints.

Let’s explore the advantages and disadvantages of hire purchase in more detail.

Advantages of Hire Purchase

When you break down the advantages and disadvantages of hire purchase system options, several clear plus points stand out for buyers. Hire purchase is commonly used for a car purchase, whether for a new or used car, allowing buyers to spread the cost over time. The car value is a key factor in determining the deposit, monthly payments and overall cost of the agreement. The finance provider plays a crucial role in managing the agreement and supporting the buyer throughout the process.

Immediate use without full payment

One of the primary hire purchase advantages is the ability to use the product immediately without having to pay the full amount up front. This can be particularly beneficial for businesses that need essential equipment to operate but may not have the necessary capital.

For example, a contractor can start using a new piece of machinery to win and deliver work, while the hire purchase payments are covered from project income. This link between asset use and repayment is a major advantage of hire purchase in financial services.

Fixed interest rates and predictable costs

Unlike some other financing methods, HP agreements typically come with fixed interest rates. This means monthly payments remain consistent, making budgeting and financial planning easier.

Knowing exactly what will be debited each month helps you manage cash flow and assess affordability. However, it’s important to note that the interest rate and monthly payment amounts can vary depending on factors such as your credit score, deposit size and contract length. For many smaller firms, this predictability is one of the most practical advantages of hire purchase system structures.

Flexibility in repayment terms

With HP, buyers often have the flexibility to choose the duration of their agreement, allowing them to adjust their monthly payments to suit their financial situation. A longer term usually means lower monthly payments but a higher overall interest cost, while a shorter term means higher monthly commitments but a lower total cost. Additionally, making a larger deposit at the start of the agreement can reduce your monthly payments and the total interest paid, making the arrangement more affordable overall.

Used wisely, this flexibility can help you match the hire purchase agreement to the working life of the asset and your expected cash flow.

Ownership after final payment

Once the final payment is made, the buyer becomes the legal owner of the asset. This means you own the car outright after making all the payments, with ownership officially transferring to you following the final payment. This is different from leasing, where the asset is returned to the lender at the end of the term.

Ownership can give you more control over how you use or dispose of the asset and may provide residual value if you sell it later. It’s one of the most important advantages of hire purchase to the buyer compared with pure rental or operating leases.

Read our article to learn more about the pros and cons of hire purchase vs. leasing business assets.

Easier approval compared to traditional loans

Businesses with limited credit history may find it easier to secure a hire purchase agreement than a traditional bank loan. The asset itself often serves as collateral, reducing the lender’s risk. Your credit rating will influence the interest rate and terms you’re offered, and having a good credit rating can help you secure better deals on a hire purchase agreement.

This can be particularly helpful for newer businesses that don’t yet tick every box for unsecured lending but still need critical equipment to grow.

Potential tax benefits for businesses

Businesses can often claim capital allowances on hire purchase assets, potentially reducing taxable profits. Some VAT-registered businesses may also reclaim VAT on the purchase, subject to the normal rules.

The exact tax treatment depends on your structure and accounting method, but for many firms, this is a meaningful advantage of hire purchase compared with some other forms of asset access. Always take specific advice.

Disadvantages of Hire Purchase

No form of finance is perfect. Understanding the disadvantages of hire purchase system arrangements is just as important as knowing the benefits. Missing payments can lead to additional fees, damage to your credit score, and even repossession of the asset. Other factors, such as your financial situation and the stability of your income, can also influence the disadvantages you may face.

Total cost can be higher

One of the main hire purchase disadvantages is that, over the length of the agreement, buyers might end up paying more than the actual value of the product because of interest charges and fees.

If you compare the cash price of the asset with the total of all instalments, the difference can be significant, especially on longer-term agreements or where the interest rate is high. It’s important to compare different hire purchase deals to understand the total cost, interest rates, and any additional fees before making a decision. This is a core disadvantage of hire purchase, you should always quantify before signing.

Ownership only after final payment

Until the final instalment is paid, the product remains the property of the seller or finance company. HP contracts and hire purchase contracts specify these terms and outline the consequences of default, such as repossession of the asset if payments are missed.

If the asset is essential to your operations, repossession can cause serious disruption. From the lender’s point of view, this secures their position, but from your point of view, it’s one of the key disadvantages of hire purchase system structures.

Commitment to fixed payments and obsolescence risk

Even if a buyer’s financial situation changes, they’re committed to the fixed monthly payments. Purchase contracts typically do not allow for easy changes or upgrades before the end of the agreement, making it difficult to adapt if circumstances change.

Unlike some leasing arrangements, hire purchase agreements don’t usually allow for easy upgrades or changes to the asset before the agreement ends. If the asset becomes obsolete, the buyer is still responsible for completing the payments. That combination of fixed commitments and product risk is an important hire purchase disadvantage to factor into your planning.

Depreciation risk sits with the buyer

If the asset, for example, a vehicle, depreciates quickly, the buyer might end up paying more than the asset’s actual worth over time. Once you’ve completed the agreement and taken ownership, you carry all the upside and downside of future value.

In sectors where equipment values can fall sharply or technology moves quickly, this can be one of the most significant problems of hire purchase from the buyer’s perspective.

Advantages and Disadvantages of Hire Purchase for Buyers and Sellers

When you look at hire purchase advantages and disadvantages, there are plenty to the seller as well as the buyer. When you look at both, the picture becomes more balanced.

For buyers, the main advantages of a hire purchase include immediate use of assets, smoother cash flow and eventual ownership. The main disadvantages of hire purchase are higher total cost, risk of repossession and exposure to depreciation. It’s essential to carefully review the original agreement to fully understand all terms, payments, deposits and obligations before committing to a hire purchase arrangement.

For sellers and finance companies, the advantages of hire purchase to the seller include more sales, interest income and security over the asset. The disadvantages of hire purchase to the seller include the risk of default, administrative costs and potential issues if assets need to be recovered and resold.

Internationally, there can also be challenges. For example, problems of hire purchase companies in India have included weak recovery processes and regulatory changes, showing that the merits and demerits of hire purchase system structures can vary by country and legal framework.

Understanding both sides of the hire purchase pros and cons helps you decide where HP should fit into your own funding mix.

Real Life Example: A Business Using Hire Purchase

How a logistics company used hire purchase to grow

Background:

A UK-based logistics startup needed to expand its fleet to meet increasing customer demand. The company required two additional delivery vans but lacked the capital to purchase them outright.

Solution:

The company entered into a hire purchase agreement with a financial institution to acquire the vans, agreeing to pay £800 per month for each vehicle over a five-year period.

Outcome:

- The company was able to start using the vans immediately, increasing its delivery capacity.

- Monthly payments were manageable and predictable, allowing the company to maintain a stable cash flow.

- After five years, the logistics company became the legal owner of the vans.

Challenges:

- The total cost of the vans, including interest, was higher than the upfront purchase price.

- If the company had faced financial difficulties, there was a risk of repossession before full ownership was transferred.

Summary:

Despite the higher overall cost, hire purchase allowed the logistics company to expand operations without a significant upfront investment. For them, the advantages of hire purchase outweighed the disadvantages, making it a viable option for immediate asset acquisition. For another business with different margins or volatility, the balance of hire purchase advantages and disadvantages might look different.

Is Hire Purchase Right for You?

Understanding the advantages and disadvantages of hire purchase is essential to determine if it’s the right choice for your needs. While it offers the benefit of immediate use, fixed payments and eventual ownership, it also comes with potential pitfalls such as higher total costs, fixed commitments and the risk of losing the product if payments aren’t met. Compared to other car finance options like Personal Contract Purchase (PCP), hire purchase doesn’t require a balloon payment at the end of the term. PCP agreements often involve a large final balloon payment to take ownership, while with hire purchase, you own the asset outright after the last regular payment, making the process more straightforward.

Ask yourself:

- Is the asset essential to generating income or productivity?

- Can you comfortably afford the payments even if trading conditions worsen?

- How quickly might the asset become obsolete or fall in value?

In the vast world of finance, where every decision can impact your financial health, it’s vital to stay informed. If your UK business requires asset finance solutions and opportunities for growth, Funding Guru is here to help. Explore our extensive resources or get in touch today. Remember, making informed choices today paves the way for a brighter financial future.

Key takeaways on hire purchase advantages and disadvantages

- Hire purchase can be a powerful way to access essential assets without large upfront payments, but the total cost is usually higher than paying cash, as you pay the full value of the asset over time.

- The main advantages of hire purchase centre on predictable repayments, asset access and eventual ownership, while the main disadvantages of hire purchase relate to fixed commitments, depreciation and repossession risk

- Weighing the hire purchase advantages and disadvantages in the context of your cash flow, risk tolerance and asset needs is the best way to decide whether HP belongs in your funding toolkit

FAQ about Hire Purchase Agreements

How can you decide if hire purchase is better than a bank loan?

You should compare the total cost, security and flexibility of each option. Hire purchase is often easier to obtain because the asset secures the agreement, and you’ll usually get fixed payments and eventual ownership. A bank loan may offer lower rates in some cases and give you more freedom over how you use the funds. To choose, look at the interest rate, fees, security, term and how important it is for you to match payments directly to asset use.

What advantages of hire purchase matter most for small businesses?

For small businesses, the biggest advantages of hire purchase are usually the low initial outlay, predictable monthly payments and the ability to start using equipment straight away. These help with cash flow and make it easier to plan. If you’re a smaller firm, the fact that the asset acts as security can also make approval more likely than for an unsecured loan.

What are the main disadvantages of hire purchase you should watch out for?

The main disadvantages of hire purchase you should be aware of are the higher overall cost compared with paying cash, the fact that you don’t own the asset until the final payment and the risk of repossession if you fall behind. There’s also the risk that the asset depreciates faster than expected, leaving you having paid more than it ends up being worth. These disadvantages of hire purchase system structures make it vital to stress test your budget before signing.

How does hire purchase affect your balance sheet and tax position?

For many businesses, hire purchase assets are treated as if you own them from the start, so the asset and the liability both appear on your balance sheet. You can usually claim capital allowances on the asset and may be able to deduct interest as a finance cost. This can be one of the advantages of hire purchase system arrangements from a tax point of view, but the details depend on your accounting method, so you should take advice from your accountant.

Can you negotiate better terms on a hire purchase agreement?

Yes, you can often negotiate several aspects of a hire purchase deal. You might be able to secure a lower interest rate, a different term length or a reduced deposit. In some cases, you can also negotiate early settlement terms. To improve your position, you should compare offers from multiple providers, understand the full cost of credit and be clear about your preferred structure before you sit down with the finance company.